Schork Oil Outlook: NatGas Bears Running Out of Steam?

By: Stephen Schork

Editor, The Schork Report

As of two weeks ago yesterday, money managers trading the Nymex Henry Hub natural gas futures were short by 207,413 contracts, i.e. approx. 207 Bcf of gas. That is enough gas to keep U.S. Steel’s furnaces aglow for the next 19 years (per the company’s 2008 annual report).

More to the point, injections into underground storage over the last 10 summers averaged 2.16 Tcf ±176 Bcf. In other words, based on the amount of gas money managers had shorted two weeks ago, they could theoretically supply 24 out of 25 cubic feet of this summer’s pending injection.

In this light, analysts at The Schork Report have repeatedly stated that bears in the natty market were vulnerable to a squeeze and we positioned our portfolio accordingly.

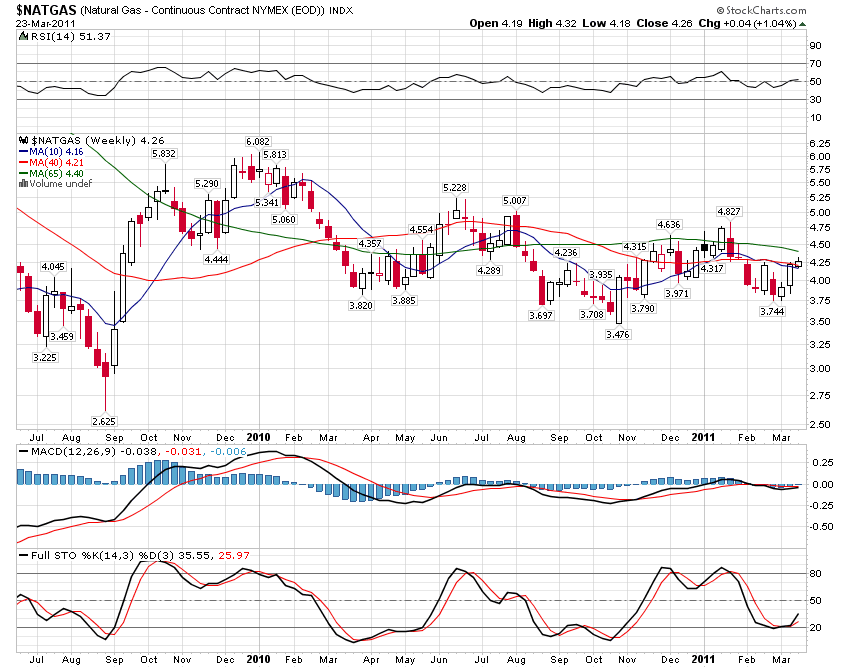

Since switching our bias to bullish as of the close of business March 09th, spot gas on the Nymex has settled higher in 7 out of 10 sessions and has climbed 12˝% (trough-to-peak). Last night the contract for April delivery finished at 4.254. That is the highest close for prompt molecules since early February.

In each day’s report to clients, we present a daily, weekly and monthly bias outlook. At the start of this trading week we stated that we would hold our short-term (daily) bullish bias and we thought a move towards the 50/62% retracement range from 4.305 to 4.440 was not an unreasonable expectation. Yesterday the contract hit a 4.269 high; the doorstep of the 50/60% range, i.e., The Box. This is the area we expect the bears to defend. A bid into the area will knock us off our bullish bias. That is to say, this seems like a reasonable area to take profit.

A push through this range clears a path towards the 4.800/5.000 area, at which point we will be interested in getting short. If on the other hand bulls stall at this point we will look for a retrace back below 4.000, at which point we have no interest in getting long.

Last October 27th, the November contract hit a 3.391 high on expiration. On the following session, October 28th, the spot December contract posted a 3.656 low; thereby creating a gap on the continuous chart.

As discussed in the March 16th issue of The Schork Report, the extant gap in crude oil (87.35 to 85.95), markets abhor gaps. Thus, the $64 questions is… if gas bears now run out of steam ahead of The Box, will they have the wherewithal to defend The Gap?