Energies

Rising inventories are taking a back seat to Middle East geopolitical concerns as tensions remain high over foreign pressure on Iran. For oil to stay flatlined during one the biggest stock market rallies in recent history is an indicator to me that this market is ready to collapse, held up only by a slight geopolitical risk premium and this stock market, which I expect to reverse and take oil down for the ride. Natural gas inventories are supposedly set to be the highest since 1983 come the end of March according to the EIA. Nevertheless this market is a buy with straight calls to play a volatility rally.

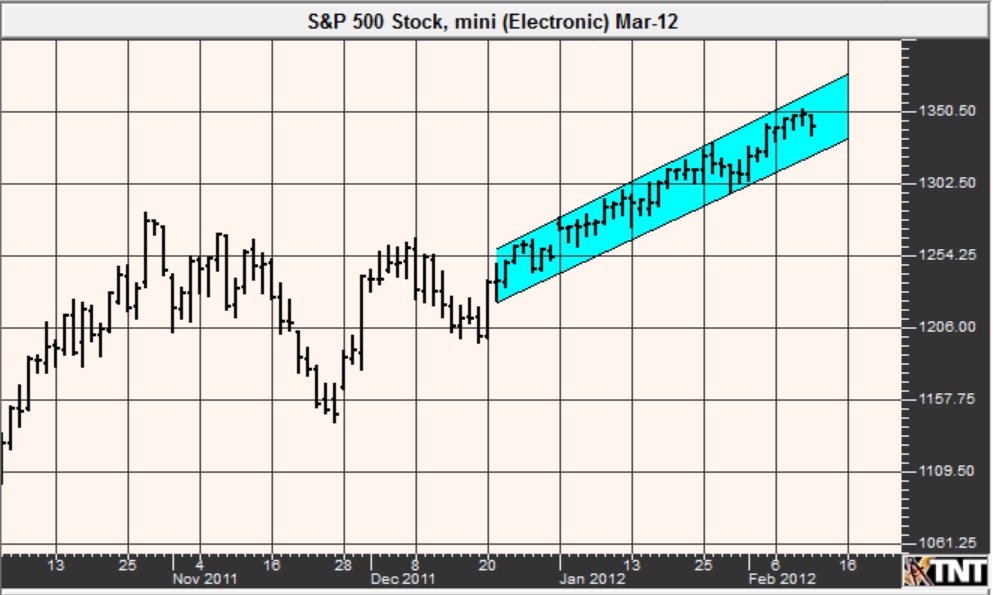

Financials

The stock market is scorching higher, continuing what is now a 13% rally since December 19th. The market has seen only 9 down closes since that time. This market is extremely overbought and I recommend continuing to accumulate put positions to capitalize on a weakening VIX, which tends to occur during sustained rallies. Bonds are a buy given their support during this rally in the stock market. When the stock market falls look for bonds to run to 150. The dollar should reverse what appears to be an overnight selloff, and I suspect this will be a big rally week in the dollar, thereby pressuring the euro currency, Canadian, Aussie and New Zealand dollars. The Japanese yen took it on the chin last week but is fast approaching key support at 128, a support that should hold. I continue to stand by my forecast that:

The Japanese Yen futures will hit 140 before it hits 80 or I will quit writing the Weekend Commodities Review...forever.

Grains

Corn’s technical turn bearish on Friday does not feel sincere and I would wait for Friday’s lows to be broken before jumping short. This should be a leading indicator for the grain sector. Wheat remains a spread buy against a short corn, while beans and rice are short plays with puts.

Report information courtesy of www.Commodinews.com

Latest WASDE: http://www.usda.gov/oce/commodity/wasde/latest.pdf

Highlights from the report:

- US wheat ending stocks are projected lower, down 25 million bushels for all wheat.

- US feed grain ending stocks are projected lower as increases in imports are offset by higher-than-expected corn exports.

- US soybean ending stock forecasts are unchanged.

Meats

Cattle reversed the previous week’s option expiration selloff, but failed again on Friday. This market is slow trending up with large one day shocks down – this is a recipe for a top. Hogs remain avoidable and sideways.

Metals

Dollar strength should pressure metals prices which have stayed at lofty levels despite strength in the stock market and fairly flat commodity prices. Bear put spreads are recommended in silver and gold. Copper should hold below last week’s high just under 3.99, otherwise this market has bullish momentum against my market views.

Softs

Cocoa appears to have reverted back into a bear market and could ultimately see substantial downside to 1500, my long term target for this market. Look for a confirming close below Friday’s low. Coffee reversed a bold rally attempt and should see fresh lows below 213 shortly. Cotton remains a short along with sugar. OJ’s failure from epic highs is not surprising as the market lacks the panic factor it had back in January – expect this to be a volatile market for the foreseeable future.

___________

James Mound

Head analyst for MoundReport.com

Disclaimer: There is risk of loss in all commodities trading. Losses can exceed your account size and/or margin requirements. Commodities trading can be extremely risky and is not for everyone. Some option strategies have unlimited risk. Educate yourself on the risks and rewards of such investing prior to trading. Past Performance is not indicative of future results. Information provided is compiled by sources believed to be reliable. JMTG or its principals assume no responsibility for any errors or omissions as the information may not be complete or events may have been cancelled or rescheduled. Options do not necessarily move in lock step with the underlying futures movement. Any copy, reprint, broadcast or distribution of this report of any kind is prohibited without the express written consent of James Mound Trading Group LLC.