Special Recap: An Excerpt from Matt's Premium Daily Wire from Friday featuring analysis of the USDA Numbers.

The trade is digesting USDA numbers as they come out with the acreage released before the opening offering wheat a reason to move lower. 58 million acres will only add to burdensome stocks domestically and internationally. This does not explain the WH-K spread moving to a 3-inverse during parts of the day. My only theory here is blow outs by late entrenched bear spreaders coupled to logistical problems backing up what appears to be a real strong basis to unattractive levels.... Beans were supported by relatively small acreage as compared with corn and wheat but a lack of front end business could cap the rally into the weekend. Improved weather outlooks for Brazil also capped the front end spread pull so be aware of spread movements today for better direction into the close. I continue to feel beans more than any other is a pit ready to roll over. This market is bloated with fresh length hoping for an explosion that the 70 MMT Brazilian crop should easily counter.

The afternoon period brought further numbers from the USDA with Ethanol the glaring figure. A ceiling has been reached concerning domestic demand so new crop corn usage fell by 50 million bushels to 4.95 billion. This is not unexpected and adds to the mild bearish undertone of the trade heading into the overnight session. The overnight was not dramatic with a mild downside tone in spite of strong crude markets. Beans closed in the upper half of the range, corn and wheat near lows while products were mixed. Meal was supported while bean oil was lower on profit taking.

Looking at the day session markets first have to digest the USDA conference balance sheets. Corn yields set at 164 bu/acre is quite hopeful I think. Harvest acreage at 87 million produces a whopping 14.27 billion!!! Ending stocks with only minor shifts to demand are estimated at 1.616 billion bushels. This is a staggering number in my eyes based solely on the huge yield estimates. If we yield 146 production is only 12.70 billion, if we meet 2010 numbers production is 13.14 billion. This is by far the largest yield expectations traders will see on the year so I say do not get overly bearish after seeing it. Estimating ending stocks right now is very similar to picking the national champion in your NCAA basketball bracket. Yes, someone hits it but it’s not normally those, “in the know”. The numbers are early estimates based on computer models, not reality of any type. They do not figure in weather, drought monitor, fertilizer costs, crop rotation, seed availability, reality, agronomy or the new crop bean/corn ratio. The last factor is at interesting level sitting at 2.29. Remember that the decision line for producers is normally 2.25 so the choice is harder by the day as seed orders are placed. The 1-1 spread (see chart below) is sitting at $7.13 reaching for the range high around 7.40. At this level look for profit taking as technical pressure adds up. The acreage battle is in full effect with plenty of time to potentially change this spread dramatically.

Outside of the USDA numbers traders saw export sales impress again with beans the obvious feature. 3 MMT old and new sales were generally expected but the loadings are still way big! 1.207 MMT shipped with China taking 676 TMT. Corn was the only number that failed to reach the upper end of estimates offering a bit more downside momentum if fundamentals were all that mattered. A higher crude market, weaker USD and an overall sentiment towards bulls should help mitigate any losses into March option expiration on the close. Look for another choppy session with end week positioning helping set the tone into the latter parts of the session. I may be cutting my teeth on the wrong side of the market but I continue to feel this trade is overinflated in the short term.... USDA baseline increased wheat acreage to 58 million, increased yield to 44.5, set production at 2.165 billion bushels which increased ending stocks to 957 million. Exports remained flat while feed usage increased as SRW moves further into cattle rations. A non impact as compared with beans and corn but this does take into account much improved expectations for the winter crop. If anything changes for the HRW into spring these numbers will shift dramatically to the bull side.

USDA baseline left beans planted acreage at 75 million as compared with last year, increased harvested acreage by 500K (How the hell do they do that?), actually increased yield marginally and increased production by 200 million bushels. The math simply does not work here in my opinion. They increased crush by 35 million bushels, increased exports by 275 million bushels which lowered ending stocks to a shocking 205 million. This is the most bullish baseline number of the big three. What if we do not increase harvested acreage? That puts ending stocks at 165 million which makes many really uneasy and changes the game moving forward. Couple this to the outlook for Argentina and China is sitting on the hot seat.

Overall the USDA offered traders a few nuggets to focus on. Look at corn acreage, corn yield, bean harvested acreage, bean exports and crush and spring wheat acreage estimates. An interesting report that leaves the trade leaning more bullish than they were just a few days ago. This also explains the expansion of the SX/CZ ratio…the acreage battle is now on!

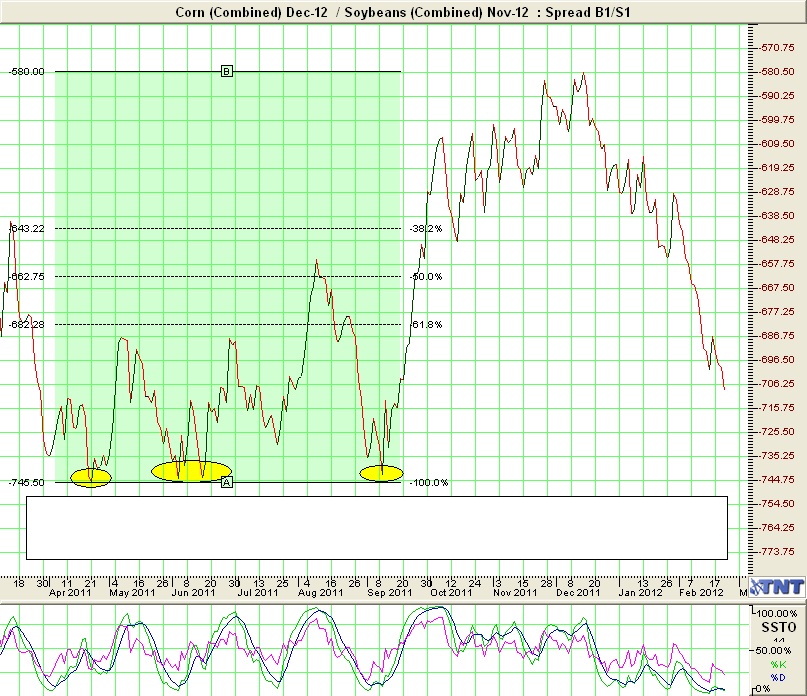

Chart:

Corn, Dec-12/Soybeans, Nov-12 - Today's USDA numbers changed the outlook for this spread. Beans likely need to fight tooth and nail for acreage so this spread could easily eclipse recent highs around 7.40, in my view. It will be a tough road with all the recent fund length likely to take profits against the range highs but fundamentals are changing quickly so I say do not load up on the bear side as this approaches 7.40. If you must be bearish....

Disclaimer: Past performance is not indicative of future results. Trading futures and options involves substantial risk of loss and is not suitable for all investors. Fundamental factors, seasonal and weather trends, daily news, and other current events may have already been factored into the markets. The use of stop loss or contingent orders may not protect profits and may not limit losses to the amount intended. Certain market conditions make it difficult or impossible to execute such orders.