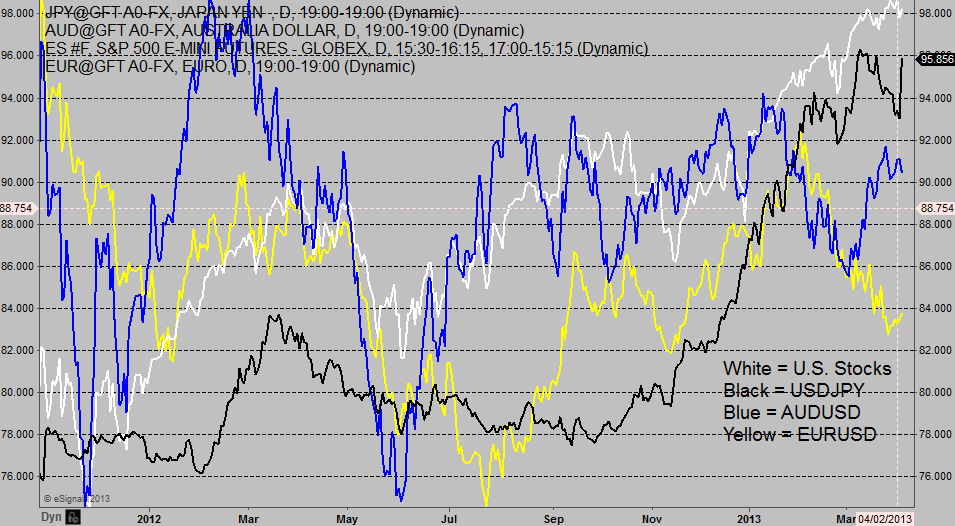

The Bank of Japan backed their earlier accommodating policies with a stimulus program set to buy 7 trillion yen (nearly $750 billion) of bonds per month. The yen plunged accordingly. We see the weak yen - strong USDJPY - as a status quo event and would look for a continuation of the price behavior we saw from mid-November thru this year with U.S. stocks, the Australian Dollar, and USDJPY each taking turns flying point - see Figure 1. The exception here is EURUSD, which will likely not enjoy the acceptance it held in the 2nd half of 2012 due to the overwhelming headwinds it faces because of its disparate membership, i.e.: its southern members. Conversely a steady pattern higher for asset class markets such as stocks and Aussie is still supportive of the Euro, and should make for a more orderly bear market for the Euro compared to currency moves over the last 5 years. Bottom line we see the sharp rally in USDJPY overnight in response to the Bank of Japan's accommodating policies as supportive for the asset markets.

Currency seasonal patterns however may not favor a sustained move higher for USDJPY - the U.S. Dollar has a rather bearish seasonal in April, while U.S. blue chip stocks have a bullish pattern in April over the last 30 years. Because of the current long-term price pattern set by underlying economics - namely coordinated central banker policies -- and those long-term seasonal patterns, we favor the Australian Dollar to join U.S. blue chip stocks and re-assume a leadership role in the chart in Figure 1. This action again will likely mean support for the Euro over the coming month.

Jay Norris is the author of The Secret to Trading: Risk Tolerance Threshold Theory. To see Jay highlight trade set-ups and signals in live markets go to Live Market Exercise.

Trading is a risky endeavor and not suitable for all investors.